Imagine getting the news that your cancer treatment — the very therapy your doctor says could save your life — won’t be covered by your insurance. For thousands of patients every year, that’s not a hypothetical. It’s a devastating reality.

One moment, you’re hopeful about a promising clinical trial, a cutting-edge therapy, or even a vital transplant. The next, you’re staring at a letter with “denied” stamped in bureaucratic language that feels like a death sentence. Just ask 59‑year‑old Deron Wells from Santa Monica, who on the eve of a lung transplant trial that could have given him a chance, his insurer Cigna pulled the plug, citing “national clinical standards.” (New York Post)

From clinical trials to essential surgeries, insurers have a powerful playbook for denying — or at least delaying — lifesaving care. And while they’re playing hardball with your health, you’re left scrambling for answers.

Why Cancer Coverage Breaks Down

1. “Not Medically Necessary” — Vague, Cost‑Driven Language

Insurers routinely reject treatments by labeling them “not medically necessary.” Tools like AI‑powered third‑party auditors sift through claims, denying everything outside a strict checklist, even when doctors urge otherwise (Vanity Fair).

2. Clinical Trials and Cutting‑Edge Care Denied

Many promising therapies—like off‑label immunotherapy or lung-transplant clinical trials—fall into a coverage gray zone. Wells’s transplant was deemed experimental despite mounting evidence in his favor.

A similar case unfolded in West Virginia, where Eric Tennant, a 58‑year‑old man battling stage 4 bile duct cancer, had already outlived expectations thanks to grueling rounds of chemotherapy. His doctors recommended a targeted, noninvasive ultrasound treatment called histotripsy to break up tumors in his liver — but his insurance company denied it, calling it “not medically necessary.” The $50,000 treatment was out of reach. The family appealed four times. All were denied.

“It’s a big mess,” said Rebecca Tennant. “They’re not accountable to anyone.”

Their story isn’t unique. Health insurers issue millions of denials every year, leaving patients trapped in an appeals process filled with long delays, disconnected decision-makers, and little oversight. Even after recent reforms, many doctors say prior authorization policies are worse than ever.

3. Standards That Lag Behind Science

New studies, newer drugs, updated survival data—the science moves faster than insurers adjust. The Wall Street Journal notes that companies “weaponize the fine print,” delaying or denying payouts even on accelerated-death benefits.

When Truly Life‑Saving Treatment Isn’t Covered

Consider the story of Tammy Morrow, a 55‑year‑old mother diagnosed with metastatic breast cancer. According to Fox News, she credits a new form of “genetically targeted fractionated chemotherapy” from Envita Medical Centers in Scottsdale with transforming her diagnosis—from terminal to cancer-free in just 21 weeks.

“I am persuaded that I would not be alive today if I had not received care at Envita,” Morrow said.

Yet this personalized therapy—despite its impressive results—was not covered by insurance. Morrow spent nearly $250,000 out of pocket, relying on a GoFundMe and a second mortgage to cover costs. Her case is a stark reminder: even treatments with dramatic, life‑saving outcomes can be denied simply because they don’t fit insurer checklists.

Who Gets Hurt Most

- Metastatic and rare cancer patients: Their best care options are often excluded.

- People pursuing clinical trials: Non-standard treatments get labeled “experimental.”

- Those requiring advanced care: Like proton therapy, targeted chemo, or transplant trials—they face intense insurer resistance.

A Spotlight on Accelerated‑Death Benefits

Life-insurance policies often include “accelerated-death benefits” allowing terminally ill policyholders to unlock funds early. But as the WSJ warns, many die trying! The 6–24 month life expectancy rule is widely exploited, with insurers working delays to avoid payouts.

Attorney Christian Lassen has seen it all:

“I’ve seen firsthand how insurers weaponize the fine print.” (WSJ)

How to Fight Back

Appeal relentlessly. Use your doctor’s voice to push back on vague denials and unclear terminology.

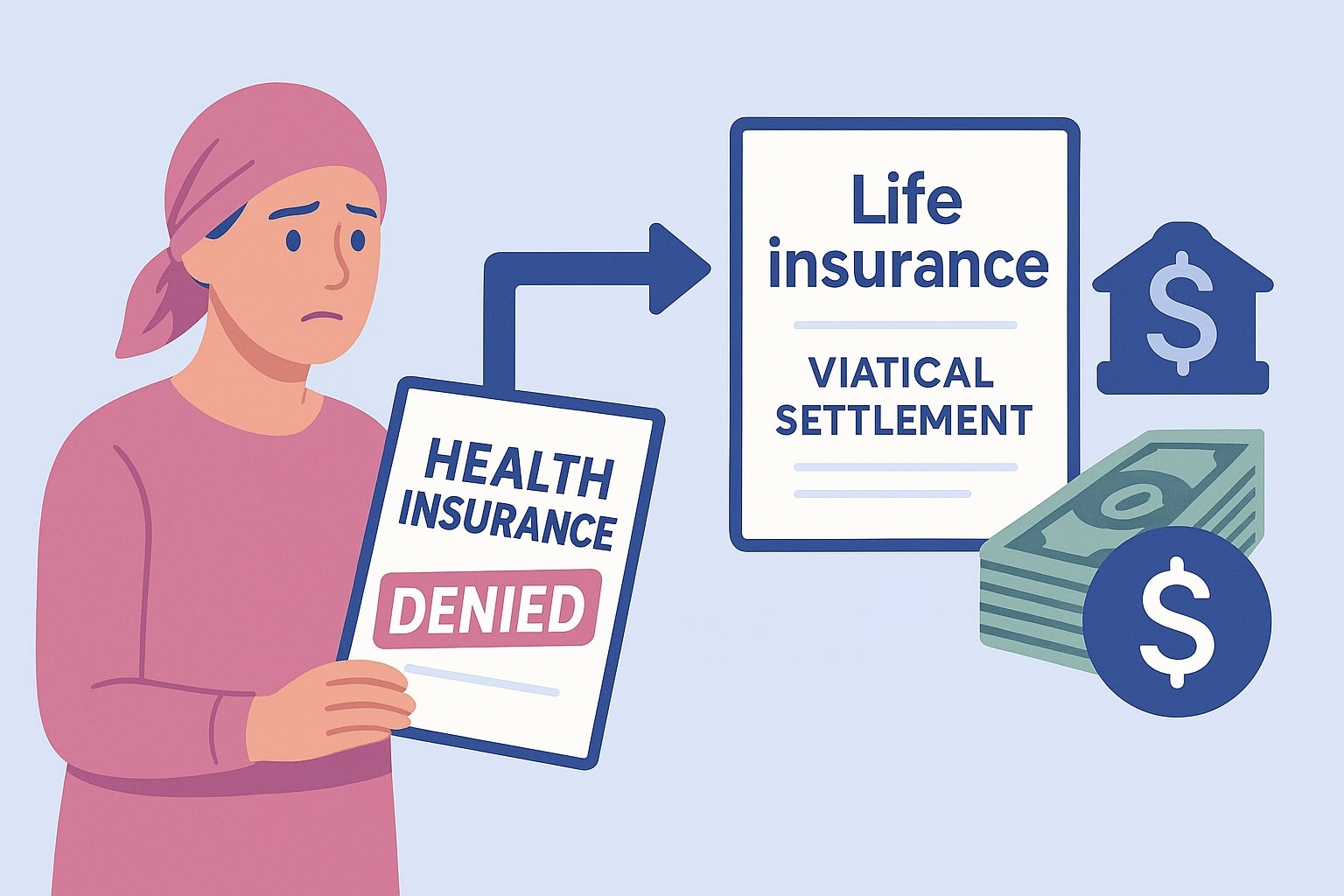

Use a viatical settlement. You can sell your life insurance policy for up to 80% of the death benefit, tax‑free, to immediately fund critical treatments. As a policy owner, your life insurance policy is an asset you own and you can sell it for cash now. No insurer red tape involved.

This is where powerful, life-changing companies such as Cancer Care Financial makes a real impact. Cancer Care Financial helps cancer patients unlock the value of their life insurance through a viatical settlement, creating previously unavailable cash to cover urgent treatment costs, living expenses, and supportive care.

They have helped many patients navigate the financial challenges of cancer with strength, dignity, and hope—providing funds in just a few short weeks.

Their specialists guide patients through the viatical settlement process, helping them unlock funds to pay for:

- Denied therapies like CAR‑T, proton therapy, clinical trials, and Envita’s targeted chemo

- Out‑of‑network cancer centers and specialists

- Supportive care, living expenses, travel, and housing

Visit www.CancerCareFinancial.com or call 844-440-7355 to speak with a compassionate specialist today.

Final Word

Insurance companies are built to deny first and appeal later, even when lives hang in the balance. But you don’t have to let their denials define your journey.

Your fight against cancer deserves every tool available—cutting-edge therapies, expert oncologists, and the financial means to choose your own path. Whether it’s the targeted chemo at Envita Medical Centers, a clinical trial at a leading hospital, or a proton therapy center across the country, you shouldn’t have to worry about how to pay for it.

By appealing denials and exploring solutions like viatical settlements with Cancer Care Financial, you can take back control. Don’t let the system dictate your options—empower yourself with knowledge, resources, and the determination to fight for the care you need and deserve.

If your insurer says no, remember: your life isn’t a line item on a balance sheet. You are a patient, a fighter, and a human being—and with the right strategies, you can get the care that’s right for you.