When cancer strikes, the physical pain is just one part of the battle. The financial burden that follows often becomes another fight—sometimes the most brutal one.

The Debt of Survival

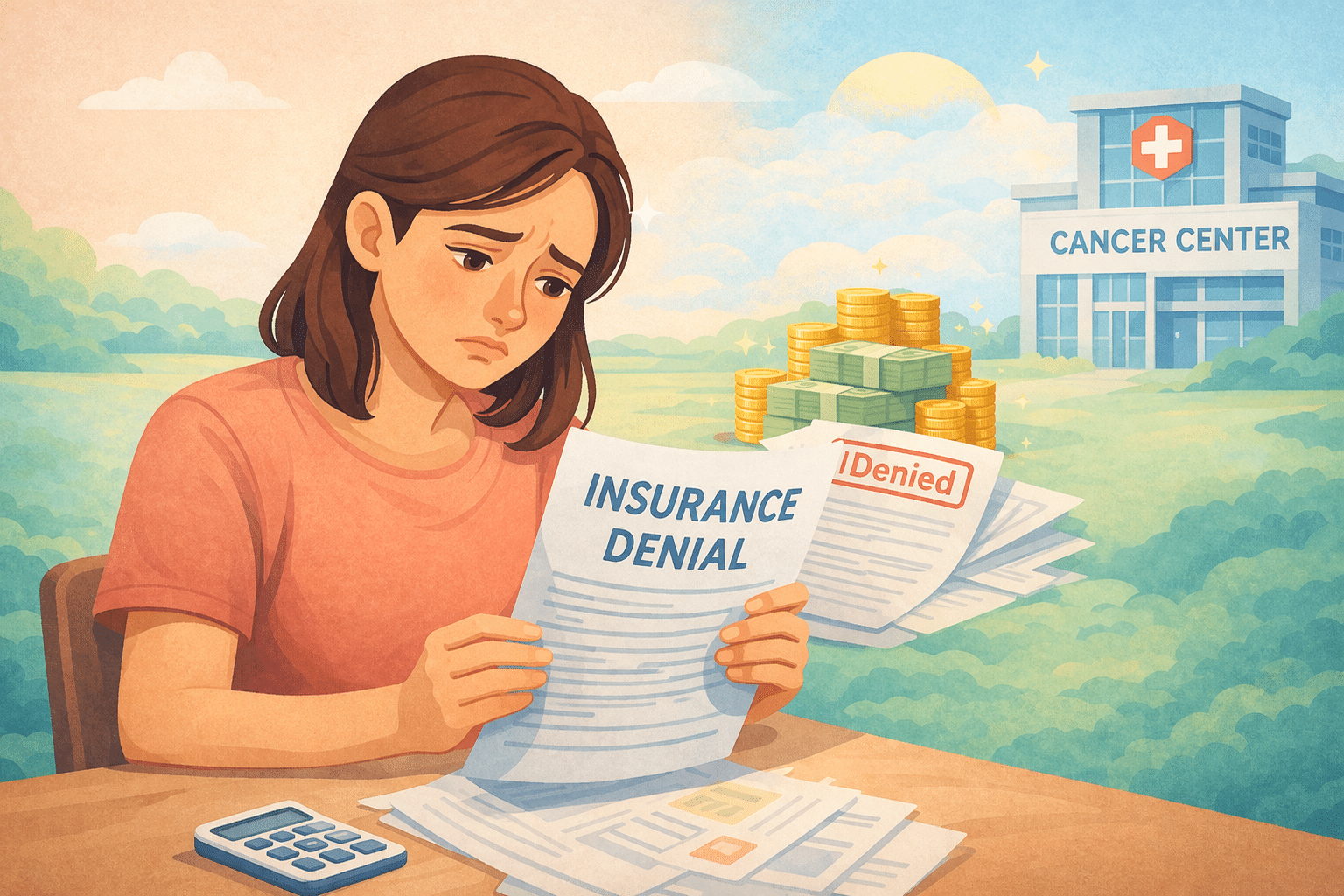

Cancer care is expensive—even when you have insurance. After a diagnosis, patients often face a cascade of bills: hospital stays, imaging, medications, surgeries, lab tests, radiation, and more. According to an investigation by KFF and NPR, the average medical and drug costs in the first year after diagnosis can run into the tens of thousands of dollars. In some cases, aggressive treatment plans push costs into the hundreds of thousands.

Even with insurance, patients end up responsible for deductibles, copays, coinsurance, out-of-network charges, and services insurers refuse to cover. For certain cancers, patients can face out-of-pocket expenses that feel impossible to manage.

One patient described waking from double mastectomy surgery only to receive a collector’s call demanding payment. Her total medical debt soon reached more than $30,000—and that was only what she knew about.

This is not rare. Many cancer patients and their families report medical debt in the tens of thousands, while some are pushed much further.

The struggle is national. Millions of Americans carry health care debt, often using credit cards, loans, or payment plans to stay afloat.

These debts ripple outwards: people skip medications, delay tests, reduce treatment intensity, drain savings, or take on extra jobs just to survive financially while fighting cancer.

Why Treatment Debt Happens (Even With “Good” Insurance)

It’s not just the “big things” like surgery. Many routine services are constrained by insurer rules. Some of the biggest cost traps include:

- High deductibles and reset limits — Every plan year, patients start over.

- Coinsurance gaps — A small percentage of a very large bill still equals a crushing payment.

- Services labeled “experimental” or “not covered” — Newer tests, integrative therapies, or interventional radiology procedures may be denied.

- Out-of-network charges — Certain specialists, labs, or radiation centers may not be covered.

- Ancillary costs — Travel, lodging, home care, lost income, and extra supportive therapies add up quickly.

When insurance says “no,” patients often have no choice but to pay—or fall into debt.

Viatical Settlements: How They Fit Into This Picture

Because medical debt is so common and dangerous, some patients look for ways outside traditional loans or fundraising. One such method is the viatical settlement.

In a viatical settlement, a patient with a serious illness sells their life insurance policy to a third party for a lump sum of cash. The buyer takes over premium payments and receives the death benefit when the insured passes.

In the context of cancer, this becomes a powerful tool:

- The funds are available quickly—you don’t wait months for appeals or approvals.

- You can use the money for anything: denied treatments, travel, integrative therapies, or daily living costs.

- There’s no repayment requirement or loan balance.

- It doesn’t cancel your health insurance—this is a separate asset being converted.

Companies like Cancer Care Financial specialize in helping patients access viatical settlements. They evaluate your policy, guide you through the process, and deliver funding in weeks rather than months. For patients facing advanced cancer and urgent medical bills, this can mean the difference between waiting and starting treatment right away.

When a Viatical Settlement Makes Sense

A viatical settlement may be a strong option when:

- Insurance denies or delays critical treatment such as interventional radiology, immunotherapy, or integrative medicine.

- You don’t have enough liquidity or borrowing power.

- You prefer not to take on additional debt.

- You need financial flexibility immediately to continue treatment.

It’s not right for everyone. The decision depends on your policy value, your health, and whether you have access to other resources such as grants or nonprofit support.

Moving Forward with Control

Medical debt robs far more than wallets—it steals peace, options, and sometimes survival.

If you are facing mounting bills and insurance refusals, it’s important to explore all possible routes. A viatical settlement is not a cure, but it can provide breathing room: turning a static life insurance policy into real financial support.

Don’t let denials or debt dictate your treatment path. Taking control of your resources may be one of the most important steps you can make.

People Also Ask

How much debt do cancer patients get into?

Many cancer patients and families report medical debts in the tens of thousands, even with insurance.

What is a viatical settlement?

It’s when you sell your life insurance policy, due to serious illness, for a lump sum of cash.

Will a viatical settlement cover denied cancer treatments?

Yes. The funds can be used for anything, including treatments insurance won’t cover.

Does selling my policy affect my insurance coverage?

No. It doesn’t cancel your health insurance—it simply converts your life insurance policy into available funds.